AI Development

- AI Services

-

-

Generative AI

Generative AI -

Data Engineering

Data Engineering -

ML Development

ML Development -

AI Consulting Services

AI Consulting Services -

Chatbot Development

Chatbot Development -

Computer Vision

Computer Vision -

Enterprise AI Development

Enterprise AI Development -

AI Agent Development

AI Agent Development -

LLM Development

LLM Development -

NLP Services

NLP Services -

RAG as a Service

RAG as a Service -

AI Integration Services

AI Integration Services -

AI Automation Agency

AI Automation Agency -

Deep Learning Development

Deep Learning Development -

AI Voice Agent Development

AI Voice Agent Development -

LLM Fine-Tuning

LLM Fine-Tuning -

Enterprise AI Chatbot

Enterprise AI Chatbot -

Vibe Coding Agency

Vibe Coding Agency -

Business Intelligence Services

Business Intelligence Services -

AI Workflow Automation

AI Workflow Automation -

AI Visual Inspection Development

AI Visual Inspection Development -

Generative AI Consulting

Generative AI Consulting -

AI PoC Development

AI PoC Development -

AI MVP Development

AI MVP Development -

Mobile App Development

Mobile App Development -

SaaS App Development

SaaS App Development -

E-commerce Development

E-commerce Development -

Web Development

Web Development -

Software Development

Software Development

AI Services

AI-Powered Engineering Services

-

- Industries

-

AI Solutions for FintechMerging AI technologies with

AI Solutions for FintechMerging AI technologies with

finance and financial services -

AI Solutions for LogisticsWe build AI solutions for

AI Solutions for LogisticsWe build AI solutions for

Logistics service providers -

Healthcare AI SolutionsWe build AI-powered

Healthcare AI SolutionsWe build AI-powered

healthcare solutions. -

Retail AI SolutionsGet robust retail AI solutions built

Retail AI SolutionsGet robust retail AI solutions built

with the latest smart retail features. -

AI Solutions for EcommerceWe build AI-powered solutions

AI Solutions for EcommerceWe build AI-powered solutions

for Ecommerce Businesses. -

AutomotiveGet apps built to track everything

AutomotiveGet apps built to track everything

from car service to fuel economy -

AI solutions for travelBuild AI- powered travel app

AI solutions for travelBuild AI- powered travel app

with all travel essential features -

AI Solutions for EducationBuild an AI-powered EdTech app

AI Solutions for EducationBuild an AI-powered EdTech app

that's fun, instructive, and insightful. -

Real Estate AI SolutionsGet AI solutions for real estate

Real Estate AI SolutionsGet AI solutions for real estate

business built with the latest features. - Hire AI Developers

-

AI Developers

AI Developers -

Gen AI Engineers

Gen AI Engineers -

Data Engineers

Data Engineers -

ML Engineers

ML Engineers -

Vibe Coding Experts

Vibe Coding Experts -

Python Developers

Python Developers -

Hire Data Scientists

Hire Data Scientists -

Prompt Engineers

Prompt Engineers

Artificial Intelligence (AI) Engineers

-

- Case Studies

- Resources

- Company

-

-

-

Table of Contents

AI in Accounting: Use Cases, Benefits, and Implementation

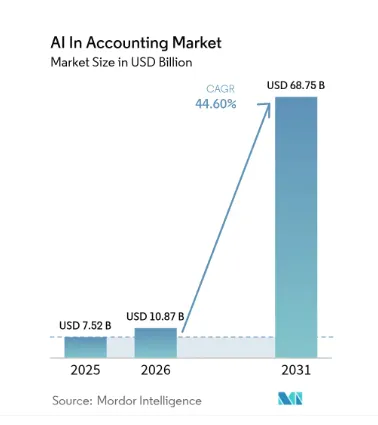

Artificial intelligence (AI) is transforming the accounting industry, enhancing financial management, decision-making, and operational efficiency. With its ability to automate complex tasks, analyze vast data sets, and streamline processes, AI is no longer a futuristic concept but a reality shaping accounting practices today. In fact, the global AI in the accounting market is expected to grow significantly, with a projected CAGR of 44.60% from 2026 to 2031, according to Mordor Intelligence. This reflects a growing reliance on AI to manage tasks such as audit automation, fraud detection, and real-time financial analysis.

However, while the adoption of AI offers numerous advantages, businesses must also navigate potential challenges. Implementing AI in accounting requires careful planning, especially around data management and security. Additionally, firms may face obstacles such as initial setup costs, the need for specialized skills, and concerns about job displacement due to automation. Despite these challenges, the long-term benefits of increased efficiency, accuracy, and the ability to generate predictive insights make AI a powerful tool for modern accountants.

As we explore the use cases, benefits, and strategies for implementing AI in accounting, it’s clear that embracing this technology can give businesses a competitive edge while reshaping traditional accounting functions.

Table of Contents

The Role of AI in Modern Accounting

Artificial intelligence plays a pivotal role in modern accounting by transforming how routine tasks are handled and enhancing data accuracy. Through the automation of repetitive processes such as data entry, invoice processing, and payroll management, AI allows accountants to focus on higher-level decision-making and strategic analysis. This shift not only reduces the risk of human error but also improves efficiency and cost-effectiveness for businesses.

One of the most significant applications of Artificial intelligence in accounting is the use of Machine Learning (ML), which enables systems to learn from historical data and make accurate predictions. For example, ML can identify patterns in financial transactions to detect anomalies and potential fraud, ensuring compliance with regulations. Natural Language Processing (NLP) is another AI technology used in accounting. NLP helps automate the extraction of valuable insights from unstructured data, such as contracts or email communications, improving the speed and accuracy of document analysis.

Additionally, Optical Character Recognition (OCR) technology plays a vital role in automating the extraction of data from scanned documents, such as receipts or invoices. OCR transforms printed or handwritten text into machine-readable formats, streamlining the data entry process for accountants. This technology not only saves time but also ensures data accuracy by eliminating manual input errors.

The role of artificial intelligence in accounting extends beyond automation. AI enhances the overall analytical capabilities of accounting systems, allowing firms to make data-driven decisions with real-time insights. By integrating AI technologies like ML, NLP, and OCR, businesses can optimize their accounting processes, reduce operational costs, and stay competitive in an increasingly data-centric world. This makes AI an essential tool in the evolution of modern accounting practices.

AI Market Statistics and Adoption Trends in Accounting

AI adoption in accounting is moving faster because finance teams want cleaner data, faster reporting, better fraud detection, and less manual work. What this really means is simple. AI in accounting is no longer limited to large enterprises. CPA firms, tax professionals, audit teams, and growing businesses now use AI accounting software for everyday tasks like reconciliation, invoice processing, tax research, audit support, and financial forecasting.

- The global AI in accounting market is growing quickly. Grand View Research estimated the market at USD 4.87 billion in 2024 and projected it to reach USD 6.71 billion in 2025. It also expects the market to grow at a 39.6% CAGR from 2025 to 2033.

- Another market estimate from Mordor Intelligence places the AI in accounting market at USD 10.87 billion in 2026 and projects it to reach USD 68.75 billion by 2031. The exact numbers vary by source, but the direction is clear. Demand for AI accounting automation is rising fast.

- AI adoption among accounting professionals has become mainstream. Karbon’s 2026 report says 98% of accounting professionals report using AI, while data security concerns have increased to 83%. This shows that firms want AI, but they also want stronger control over privacy, client data, and safe usage.

- Tax and accounting professionals expect AI to reshape their work. Thomson Reuters found that 77% of respondents believe AI will have a high or transformational impact on their work within five years, while 84% of tax and accounting professionals see AI as a force for good.

- Generative AI adoption is still growing in tax firms. Thomson Reuters reported that 21% of tax firms already use GenAI, while 53% are either planning to use it or considering it. The share of firms with no GenAI plans dropped from 49% in 2024 to 25% in 2025. (Note here that 2026 numbers are yet to come. We will update it as soon as we are available)

Quick Overview: Benefits of AI in Accounting

Here’s a quick overview of the major benefits of AI in accounting.

| Benefit of AI in Accounting | What It Means | Business Impact |

|---|---|---|

| Automation of repetitive accounting tasks | AI can handle time consuming tasks like data entry, invoice processing, expense categorization, and bank reconciliation. For example, AI tools can process hundreds of invoices in minutes and reduce the need for manual entry. | Accounting teams save time, close books faster, and spend more energy on financial analysis, planning, and business advisory work. |

| Improved data accuracy and fewer errors | AI accounting software can review large volumes of financial data with strong accuracy. It can spot duplicate entries, missing values, wrong classifications, and unusual numbers before they affect reports. | Businesses get cleaner financial records, fewer reporting errors, and better confidence in bookkeeping, tax filing, and financial statements. |

| Real time financial insights | AI can process accounting data as transactions happen. This gives businesses a live view of cash flow, revenue, expenses, payables, receivables, and financial trends. | Decision makers do not need to wait for month end reports. They can track financial health, adjust budgets, and respond faster to business changes. |

| Better fraud detection and risk management | AI can monitor transactions and detect unusual patterns that may point to fraud, duplicate payments, policy violations, or financial risk. | Businesses can catch suspicious activity early, reduce financial losses, and strengthen internal controls. |

| Cost savings and easy scalability | AI reduces manual effort and helps accounting teams manage growing data volumes without adding more people for every new workload. | Businesses can lower operational costs and scale accounting processes as transactions, clients, or locations increase. |

| Stronger client advisory services | When AI handles routine accounting work, accountants can spend more time on tax planning, cash flow advice, financial forecasting, and business strategy. | Accounting firms and finance teams can offer more valuable guidance, improve client relationships, and move from number checking to decision support. |

Key Benefits of AI in Accounting

Artificial intelligence (AI) offers significant advantages in the accounting industry by automating tasks, improving accuracy, and delivering valuable insights. Below are the key benefits of AI in accounting and how they impact businesses.

Automation of Repetitive Tasks

AI excels at automating time-consuming tasks such as data entry, invoice processing, and bank reconciliation. This automation reduces the workload on human accountants, allowing them to focus on more strategic activities like financial analysis and advisory services. For example, AI tools can process hundreds of invoices in minutes, ensuring accuracy and freeing accountants from manual entry.

Impact: The automation of repetitive tasks leads to increased operational efficiency and faster processing times. Additionally, it reduces the risk of human error, ensuring that businesses can trust the accuracy of their financial data. This enables accountants to shift their focus to higher-value work, such as strategic decision-making.

Improved Data Accuracy and Reduced Errors

AI-powered algorithms can analyze vast amounts of financial data with unparalleled precision, minimizing the likelihood of errors in bookkeeping, tax filing, and financial reporting. When handling large datasets manually, mistakes are bound to happen, but AI ensures that such errors are significantly reduced.

Impact: With improved data accuracy, businesses can make better financial decisions and enhance compliance with regulations. The reduced number of errors in financial statements leads to fewer discrepancies, which is essential for maintaining trust and credibility in business operations.

Real-Time Financial Insights

One of the most potent advantages of AI in accounting is its ability to provide real-time insights. AI systems can process financial data instantly, giving businesses a clear picture of their cash flow, expenses, and revenues at any given moment. This continuous access to data allows companies to make more informed decisions without waiting for month-end reports.

Impact: Real-time insights enable better financial forecasting and trend analysis. Businesses can react quickly to changes in the market, make timely adjustments to their financial strategies, and ultimately gain a competitive advantage in their industry.

Enhanced Fraud Detection and Risk Management

AI’s capability to detect anomalies in financial data makes it a crucial tool for fraud detection and risk management. By continuously monitoring transactions, AI can identify unusual patterns or behaviors that may indicate fraudulent activity. This early detection can prevent financial losses and maintain the integrity of the accounting process.

Impact: AI-driven fraud detection enhances financial security by identifying potential threats before they escalate. It also ensures compliance with regulatory requirements, reducing the risk of fines or penalties related to fraudulent activities or financial mismanagement.

Cost Savings and Scalability

AI’s automation capabilities directly translate into cost savings for businesses. By reducing the need for manual labour and minimizing errors, AI allows companies to lower their operational costs. As financial data volumes increase, AI solutions can scale effortlessly, managing larger datasets without the need for additional resources.

Impact: AI offers businesses the flexibility to grow without proportional increases in staffing or operational expenses. This makes AI an attractive and cost-effective solution for companies of all sizes, particularly those aiming for scalability.

Better Client Advisory Services

With routine tasks handled by AI, accountants can dedicate more time to offering value-added services such as financial consulting, tax planning, and strategic advisory. Additionally, AI can analyze client data to provide personalized insights and recommendations, elevating the quality of service.

Impact: By delivering tailored, data-driven advice, accountants can strengthen relationships with their clients and enhance client satisfaction. This transition from number-crunchers to strategic advisors helps accountants provide more meaningful contributions to their clients’ financial success.

Quick Overview: AI Use Cases in Accounting

| AI Use Case | How It Works | Business Impact |

|---|---|---|

| Automated data entry and reconciliation | AI uses OCR and machine learning to read invoices, receipts, bank statements, and financial documents. It extracts data and matches it with accounting records automatically. | Reduces manual work, improves accuracy, speeds up reconciliation, and helps accounting teams close books faster. |

| Fraud detection and risk management | AI monitors transactions and detects unusual patterns, duplicate payments, abnormal vendor activity, and suspicious entries. | Helps businesses catch financial risks early, reduce losses, improve internal controls, and stay audit ready. |

| AI powered auditing | AI reviews large volumes of financial records, documents, and transactions. It flags inconsistencies, missing details, and areas that need human review. | Saves audit time, reduces manual errors, improves audit quality, and allows auditors to focus on risk analysis. |

| Tax compliance and regulatory management | AI supports tax calculations, tax rule checks, document review, and compliance workflows. It can help teams stay aligned with changing tax requirements. | Reduces filing errors, lowers compliance risk, and helps businesses avoid penalties or missed tax obligations. |

| Financial forecasting and predictive analytics | AI studies historical financial data, current trends, cash flow patterns, and business performance to predict future outcomes. | Helps businesses plan budgets, manage cash flow, forecast revenue, and make better financial decisions. |

| Client management and advisory services | AI organizes client data, tracks communication, prepares reports, and generates personalized financial insights. | Helps accounting firms offer better advisory services, improve client relationships, and deliver more value beyond basic reporting. |

| AI powered audit support | AI scans supporting documents, cross checks records, reviews compliance gaps, and highlights data that needs deeper attention. | Makes audit support faster, more accurate, and more useful for risk review, compliance checks, and financial advisory. |

AI Use Cases in Accounting

AI is revolutionizing accounting through various applications that streamline operations, improve accuracy, and offer real-time insights. Below are key use cases of AI in accounting and how it solves critical challenges in the industry.

Automated Data Entry and Reconciliation

Problem: Traditional data entry and reconciliation processes are time-consuming, prone to human error, and resource-intensive. Accountants often spend hours manually entering data from receipts, invoices, and bank statements, followed by tedious reconciliation with accounting records.

AI Solution: AI tools such as Optical Character Recognition (OCR) and Machine Learning (ML) automate data extraction from documents like invoices and bank statements. Once extracted, AI algorithms automatically reconcile these records with the company’s accounting system, reducing the potential for errors and speeding up the process.

Example: A mid-sized accounting firm implemented AI-powered automation to handle repetitive tasks such as reconciling client accounts. This led to a 40% reduction in processing time while significantly improving the accuracy of data, allowing the firm to focus on more complex financial analysis.

Fraud Detection and Risk Management

Problem: Detecting fraudulent activities or errors in large datasets can be inefficient when done manually, often leading to missed risks or delayed detection of issues.

AI Solution: AI can detect irregularities and potential fraud by continuously monitoring financial transactions and identifying patterns. It uses advanced algorithms to recognize anomalies that deviate from typical behavior, allowing early detection of suspicious activities and reducing risks.

Example: Tools like MindBridge and Trullion use AI to monitor transaction data in real-time, flagging discrepancies that could indicate fraudulent behavior. These systems help businesses reduce financial risks by identifying potential fraud early on and ensuring compliance with internal policies.

AI-Powered Auditing

Problem: Traditional auditing is labor-intensive, requiring manual verification of records, extensive documentation review, and time-consuming cross-checking for compliance.

AI Solution: AI automates large portions of the auditing process by analyzing vast amounts of data in real-time. This allows auditors to focus on interpreting results rather than manually verifying each record. AI systems can flag potential compliance issues or irregularities, making the audit process more accurate and efficient.

Example: Companies like Deloitte and PwC have integrated AI into their auditing processes to sift through massive volumes of documents, flagging inconsistencies and improving audit speed. This not only saves time but also increases the overall quality of audits by reducing manual errors.

Tax Compliance and Regulatory Management

Problem: Keeping track of ever-changing tax regulations and ensuring compliance, especially for global enterprises, can be a complex and challenging task.

AI Solution: AI platforms can interpret and apply complex tax codes, automating the tax preparation and filing process. These systems are regularly updated with the latest tax laws and regulations, ensuring that companies remain compliant while minimizing errors.

Example: AI-driven tax software like Avalara or Xero automates tax calculations, updates with current tax laws, and even handles return filing. This ensures businesses remain compliant with the latest regulations, reducing the risk of penalties or audits.

Financial Forecasting and Predictive Analytics

Problem: Traditional financial forecasting methods often rely on manual analysis, which can be inaccurate due to limited data or outdated methods.

AI Solution: AI uses predictive analytics to provide accurate financial forecasts by analyzing historical data and real-time financial trends. AI models can assess vast amounts of data to predict future revenue, expenses, and market behavior with a higher degree of accuracy.

Example: AI tools such as Adaptive Insights or Oracle Financials enable businesses to generate more precise financial forecasts. These tools exemplify the applications of AI in business, as they predict cash flow and market performance, helping businesses make informed financial decisions and adjust strategies based on anticipated trends.

Enhanced Client Management and Advisory Services

Problem: Accountants spend significant time manually tracking client needs, processing routine requests, and generating personalized reports, which limits their ability to scale operations.

AI Solution: AI-powered customer relationship management (CRM) systems allow accountants to manage client data more efficiently. These systems can automate reports, generate insights, and track communication, giving accountants more time to focus on high-value advisory services.

Example: Firms like KPMG use AI-driven CRM systems to offer proactive, data-backed advice to clients. This enhances their consulting services, allowing them to provide more personalized and strategic recommendations, leading to improved client satisfaction and stronger relationships.

AI-Powered Audit Support

Problem: Auditing often involves complex, labor-intensive tasks that demand the manual review of numerous documents and financial records, leading to inefficiencies.

AI Solution: AI-powered auditing systems automate many of these tasks, helping auditors quickly sift through large amounts of data and highlight areas that require attention. These systems also cross-check compliance issues, making audits faster, more accurate, and less resource-intensive.

Example: Audit firms use AI solutions to enhance their auditing processes by reducing manual effort and improving the accuracy of findings. These AI systems allow auditors to focus on more critical tasks like interpreting data and advising on risk management strategies.

By leveraging AI, accounting processes become more efficient, scalable, and accurate, positioning businesses to succeed in a data-driven environment.

How to Implement AI in Accounting System

Implementing AI in accounting requires a structured approach, aligning technology with business objectives. Below are the key steps to ensure a successful AI integration into accounting processes.

Define Objectives and Use Cases

Before integrating AI, it’s crucial to define the specific goals and use cases that will drive its adoption in accounting. Start by identifying areas where AI can create the most value, such as automating data entry, improving audit accuracy, or enhancing fraud detection. This step ensures that AI implementation is aligned with business objectives and provides measurable outcomes.

For example, if your objective is to reduce the time spent on manual tasks, you could focus on AI tools that automate invoice processing or bank reconciliations. Clear objectives help in selecting the right AI solutions and optimizing their use across different accounting functions. Engaging with experts offering AI Development Services can assist in identifying tailored use cases that meet your business needs.

Data Collection and Preparation

Once objectives are set, the next step is gathering the necessary data. AI relies heavily on large sets of accurate data to function effectively. For accounting, this could include financial transactions, invoices, bank statements, and tax records. It’s important to clean and prepare this data, ensuring it is free of inconsistencies and errors.

Data preparation often involves organizing the data into structured formats that AI systems can easily interpret. Additionally, consider any gaps in data that need to be addressed before proceeding with AI model training. Proper data preparation is the foundation for successful AI implementation, as it improves the system’s ability to make accurate predictions and automate processes.

Data Security and Compliance

With the integration of AI, maintaining data security and ensuring compliance with relevant regulations become critical. Accounting firms deal with sensitive financial data, and any breach could result in severe financial and reputational damage. Therefore, it’s essential to implement robust security measures that protect this data while complying with industry standards like GDPR or CCPA.

Encrypting data, setting up secure access protocols, and using AI systems that are compliant with regulations are necessary steps. Furthermore, businesses must conduct regular audits to ensure that AI systems are not only secure but also meet legal and ethical requirements. Compliance should be integrated into the AI solution to avoid legal risks associated with mishandling financial data.

AI Model Development and Training

Once data is prepared, the next step is developing and training the AI models. This involves selecting appropriate algorithms and training the AI on historical data. The AI learns from patterns in the data to make accurate predictions, automate tasks, and generate insights. For example, machine learning models can be trained to recognize anomalies in financial transactions or predict future cash flows based on past data.

Training is an ongoing process, as the model continually improves as it processes more data. It’s essential to periodically update the training data to reflect current trends and ensure that the AI system remains effective over time.

Integration with Existing Systems

To maximize AI’s benefits, it’s crucial to integrate the AI system with your existing accounting software and infrastructure. This allows for seamless data flow between systems and minimizes disruptions to current workflows. Whether you are using ERP systems, payroll software, or other accounting tools, the AI solution should work in harmony with these platforms.

Speaking from a perspective where making a WMS project successful in the least possible time is the priority, minimizing customization can be a key factor. Leveraging project management software can further streamline implementation by improving coordination, tracking progress, and ensuring teams stay aligned throughout the process.

Integrating AI with existing systems also improves efficiency, as data does not need to be manually transferred between platforms. This step reduces human intervention, improves data accuracy, and enables real-time updates across all systems.

Also read : AI in Software Development: A Comprehensive Guide

Testing and Validation

Before fully deploying AI in accounting, it’s important to thoroughly test the system to ensure that it works as expected. Testing involves evaluating the AI’s performance on key metrics such as accuracy, speed, and efficiency. It also includes validating that the system complies with security protocols and regulatory standards.

Conducting pilot programs can be an effective way to test AI’s impact on accounting processes in a controlled environment. During this phase, feedback from accountants and financial teams is critical to refine the AI system and make any necessary adjustments before full-scale implementation.

Continuous Monitoring and Improvement

AI implementation does not end with deployment. Continuous monitoring and improvement are necessary to ensure the system remains effective over time. Regularly reviewing AI’s performance, monitoring key metrics, and updating the model based on new data are essential for keeping the system optimized.

Businesses should also stay updated on advancements in AI technology, incorporating new features or tools that can further enhance accounting processes. By continuously refining the system, businesses can ensure that AI continues to deliver value and adapt to changing business needs.

Overcoming Challenges of AI Implementation in Accounting

Implementing AI in accounting comes with its own set of challenges, from data security concerns to the cost of implementation and the resistance from employees. Addressing these obstacles is crucial for ensuring a smooth transition and reaping the full benefits of AI in financial processes.

Data Security and Privacy Concerns

One of the biggest challenges in AI implementation for accounting is ensuring data security and privacy. Given the sensitive nature of financial information, it is essential that AI solutions comply with regulations such as the General Data Protection Regulation (GDPR) and other financial data protection laws. Failing to secure data can result in costly breaches, fines, and a loss of trust from clients.

To address this, businesses should implement AI systems that use robust encryption methods, ensuring that data is protected both at rest and in transit. AI tools must also be regularly audited to confirm compliance with relevant regulations. In addition, ensuring that data access is restricted to authorized personnel helps minimize the risk of internal breaches. Proper compliance management is not just about meeting regulatory requirements, but also about maintaining the security and integrity of accounting data.

Cost of Implementation

Another challenge is the cost of implementing AI in accounting. From initial setup to training, testing, and integration with existing systems, the financial investment required can be substantial. Businesses need to evaluate the costs against the expected return on investment (ROI). Calculating ROI includes not only the immediate savings from automating tasks but also long-term benefits like improved accuracy, reduced errors, and the ability to scale without significantly increasing labor costs.

To justify the investment, it is essential to create a detailed cost-benefit analysis. This should include direct costs (hardware, software, and employee training) as well as indirect savings (time saved, reduction in manual errors, and enhanced productivity). While the upfront costs may be high, the long-term benefits in terms of efficiency and accuracy make AI a cost-effective solution for many businesses. Demonstrating these benefits helps secure leadership buy-in and justifies the initial expenditure.

Resistance to Change

Lastly, resistance to change is a common issue when implementing AI in accounting. Many accountants and financial staff may feel threatened by the idea of AI taking over their roles or may simply be uncomfortable with new technology. This resistance can slow down implementation and limit the overall effectiveness of AI.

To overcome this, businesses should focus on educating their teams about the role of AI as a tool to enhance their capabilities rather than replace them. Training programs that teach employees how to work alongside AI systems can reduce fear and hesitation. Additionally, highlighting the benefits of AI—such as reduced workload for repetitive tasks and the ability to focus on higher-value activities—can help staff see AI as an enabler of growth and efficiency. Engaging employees in the AI adoption process and seeking their feedback can also make the transition smoother.

By addressing these challenges head-on, businesses can create a more positive environment for AI implementation, ensuring that both the technology and the people using it thrive.

Ensuring Compliance and Ethical Considerations

When implementing AI in accounting, ensuring compliance with regulations and addressing ethical considerations are critical. These factors are essential for maintaining trust and transparency in AI-driven processes.

Regulatory Compliance

Incorporating AI into accounting processes requires strict adherence to industry standards such as the International Financial Reporting Standards (IFRS) and Generally Accepted Accounting Principles (GAAP). These frameworks provide guidelines that ensure consistency, accuracy, and transparency in financial reporting. For AI to be effective in accounting, it must be designed and programmed to follow these standards closely.

AI systems used in accounting should automate processes like financial reporting, audit preparation, and reconciliation, while staying compliant with regulations. For example, AI-driven tools must correctly apply IFRS and GAAP standards to ensure the financial reports they generate align with legal requirements. Regular audits of the AI systems are necessary to verify their accuracy and compliance with these standards. Additionally, AI systems should be updated regularly to reflect changes in accounting laws and regulations, ensuring that businesses maintain compliance as these guidelines evolve. By adhering to these standards, AI can enhance the reliability and transparency of financial data.

Ethical Considerations in AI Usage

When using AI in accounting, it’s important to address the ethical concerns surrounding AI decision-making. One significant concern revolves around the clarity and interpretability of AI algorithms. Since AI systems make decisions based on complex data models, it can be challenging to understand how these decisions are made, leading to potential issues of accountability. In the context of accounting, where transparency and trust are paramount, ensuring that AI decisions are explainable and traceable is crucial.

Additionally, businesses must consider the ethical implications of AI when it comes to data privacy and biases in decision-making. For instance, AI systems that analyze financial data must protect sensitive client information and adhere to ethical standards regarding data usage. There is also a risk of AI unintentionally reinforcing biases in financial predictions, which could impact the fairness of financial reporting or auditing practices. To mitigate these risks, businesses should establish clear guidelines for AI usage and ensure that their AI models are regularly reviewed for bias, accuracy, and transparency. Implementing ethical AI systems not only ensures compliance with regulations but also fosters trust among clients and stakeholders.

By addressing both regulatory and ethical concerns, businesses can integrate AI into their accounting processes in a way that enhances trust, transparency, and accountability.

Future Trends in AI-Driven Accounting

As AI continues to advance, its impact on the accounting industry will expand, introducing new trends that further transform financial processes. Below are key future trends in AI-driven accounting and how they will shape the industry’s evolution.

Continuous Auditing and Real-Time Reporting

AI is set to revolutionize the future of auditing by enabling continuous audits and real-time financial reporting. Traditionally, audits have been periodic, conducted annually or quarterly. However, with AI, businesses can move toward continuous audits, where financial transactions are monitored and verified in real-time. This shift allows for faster identification of discrepancies or fraud and ensures that financial records remain accurate throughout the year, rather than waiting for an audit at the end of the reporting period.

Real-time reporting is another trend that AI will continue to enhance. AI systems can automatically generate reports as transactions occur, giving businesses instant insights into their financial health. This capability enables companies to make timely decisions based on up-to-date financial data. For example, cash flow analysis or expense tracking can be done in real-time, allowing businesses to respond quickly to financial challenges or opportunities.

With continuous auditing and real-time reporting, companies can maintain a higher level of financial transparency and compliance, which is crucial in today’s fast-paced business environment.

Blockchain and AI Integration

The integration of AI and blockchain represents a powerful combination for enhancing transparency and fraud prevention in accounting. Blockchain’s decentralized ledger system ensures that financial transactions are recorded in an immutable and tamper-proof manner, while AI’s capabilities in analyzing large datasets can be leveraged to monitor these transactions continuously.

When combined, AI can scan blockchain records for patterns or anomalies that may indicate fraud or errors, providing an additional layer of security. This integration is particularly promising for tasks such as verifying financial transactions, auditing, and ensuring compliance with regulations. Blockchain’s ability to create a transparent and traceable financial record, along with AI’s capacity for quick data analysis, offers immense potential for reducing fraud and enhancing the accuracy of financial reporting.

As more businesses adopt blockchain technologies, the role of AI will become increasingly important in making sense of the vast amounts of data generated, helping to identify potential risks and ensuring that financial records remain secure and trustworthy.

AI’s Role in Financial Advisory

AI is poised to play a significant role in financial advisory services, helping accountants provide better, more data-driven advice to clients. Currently, AI tools assist with automating tasks such as financial forecasting and data analysis. In the future, these tools will evolve to become even more sophisticated, offering predictive insights that can inform strategic financial decisions.

AI-driven advisory services will allow accountants to analyze large datasets, identify trends, and offer personalized recommendations to clients in real-time. For example, AI can assess a client’s financial history, market conditions, and economic forecasts to offer tailored investment strategies or tax planning advice. This will enhance the accountant’s ability to serve as a strategic advisor, rather than just a number-cruncher.

As AI becomes more integrated into financial advisory services, accountants will have the tools to offer deeper insights and more personalized recommendations, improving the value they provide to their clients and helping businesses make smarter financial decisions.

Conclusion

Implementing Artificial intelligence in accounting is a transformative journey that begins with careful planning and clear objectives. By following the key steps—defining use cases, preparing data, ensuring security, and integrating AI software into existing systems—businesses can successfully incorporate AI into their financial operations. Starting small with targeted AI applications, such as automating data entry or enhancing fraud detection, is an effective approach. This allows businesses to experience immediate benefits and gradually scale AI adoption as they become more comfortable with the technology.

It is also important to continuously monitor and refine AI systems to ensure optimal performance. Staying updated on emerging trends in AI, such as real-time reporting, blockchain integration, and AI-powered financial advisory services, will help businesses stay competitive in a rapidly evolving landscape. Partnering with experts, such as Prismetric, the best AI development company in Australia, can further support businesses in smoothly navigating this transition.

By embracing AI technology, businesses can not only improve efficiency and accuracy but also position themselves as leaders in innovation. The future of accounting lies in the strategic integration of AI, and taking incremental steps now will set the stage for long-term success in the industry.

As the tech-savvy Project Manager at Prismetric, his admiration for app technology is boundless though!He writes widely researched articles about the AI development, app development methodologies, codes, technical project management skills, app trends, and technical events. Inventive mobile applications and Android app trends that inspire the maximum app users magnetize him deeply to offer his readers some remarkable articles.

Our Recent Blog

Know what’s new in Technology and Development

14+Years’ Experience in IT

Prismetric Success Stories

0+

Happy Clients

0+

Solutions Developed

0+

Countries

0+

Developers